what percentage of salary should go to savings

Forget about the adept old days when you lot could rely on an employee pension plan and Social Security to encompass the cost of your retirement years. Today'southward economy requires a well-laid-out retirement programme.

Unfortunately, saving for retirement isn't a one-size-fits-all kind of process. Everyone's situation is unique and, as such, you need to observe a retirement account that best caters to your private job situation and retirement goals. Here's a guide to help you find the all-time retirement savings accounts to secure your future.

Some people will call information technology a retirement savings programme, others will call it a retirement savings program, information technology doesn't really matter. All these terms are coined to represent a place and a strategy for putting some coin aside before retirement to help you with expenses in the hereafter.

This may seem like an all-too-early affair to do, especially if you are younger, just truth be told, it's never besides early to secure your future. Besides, having a retirement savings business relationship gives you access to a tax-deferred retirement account, which volition reduce the taxes you pay. How is that for motivation?

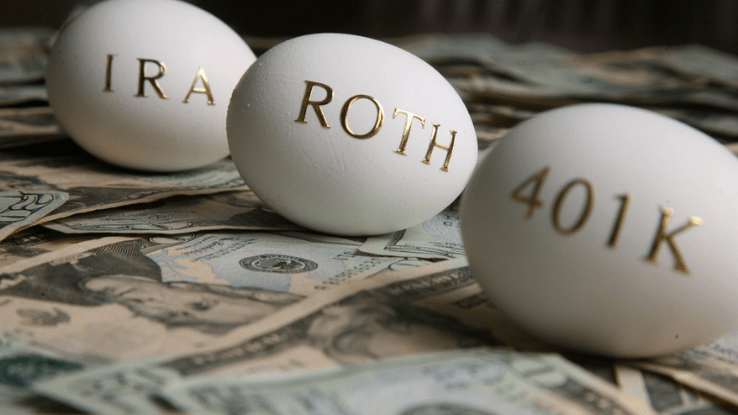

Types of Retirement Savings Accounts

Now that you know what a retirement savings account is, and why y'all'd exist better off having one, you are fix to delve into the different types of accounts available. At first, these unlike types of accounts may appear overwhelming, or maybe a scrap disruptive. Just, cypher a skilful simple caption won't fix so let'southward begin. Afterward nosotros introduce some of the options bachelor, we'll count down five of the best.

one. The 401(thousand)

Sounds familiar? That's probably because it is one of the most mentioned retirement savings accounts in the United states of america. A 401(grand) business relationship is obtained through employers. This means you have to be employed to get your 401(k) account, but not every workplace offers this plan.

When it comes to contributions, the IRS allows you lot to put in at most $19,500 to your 401(grand) business relationship if you lot are beneath 50 years old. In case you are 50 or older, then you lot can put up to $26,000 in your account. Ultimately, you can start making over-the-counter withdrawals from the account once you turn 72 years onetime. Penalties may apply if you try to withdraw before age 59 and a half.

2. Solo 401(one thousand)

What near cocky-employed individuals, do they get retirement saving plans? Yep, they do. These are known as Solo 401 (k) or 1-participant 401(k) plans. This account is eligible for an individual business owner who has no employees. The IRS allows y'all contributions of upwardly to $58,000. For people aged fifty or older, catch-upwards contributions of upwards to $6,500 are allowed.

three. 403(b)

In case you work for nonprofit or tax-exempt organizations you can also plan for your retirement through the 403(b) account. It comes with the same contribution limitations as a 401(k) plan and lets your earnings abound tax-costless until yous commencement withdrawing, at which signal the amounts withdrawn are subject to income tax.

4. IRA

In total, "IRA" means "private retirement account". This is a retirement savings plan available only for people with earned income. Earned income refers to all the taxable income and wages obtained from work or certain inability payments. IRA's contribution limit is $vi,000 or $7,000 if you are 50 or older, and the funds you lot withdraw become taxable income. IRAs also come in other variants like self-directed IRAs, and SIMPLE IRAs and SEP IRAs that cater to self-employed individuals or business owners with few employees.

5. Roth IRA

For Roth IRA, y'all must also have earned income. The contribution and historic period limits are also like to IRAs. The only deviation is that with a Roth IRA, you take to pay taxes on the amount y'all contribute. All the same, at the time of withdrawal, the money you withdraw will be tax-free. As much equally this retirement savings business relationship comes with an impressive tax benefit, the eligibility to contribute to it is fully dependent on having earned income. As well, it simply offers y'all tax savings if y'all have a higher tax rate in retirement.

6. Thrift Savings Programme

The Thrift Savings Plan (TSP) is quite similar to the 401(k) plan. The only departure is, information technology'due south available to government workers and members of the uniformed services only.

Should you be eligible, you will cull to put your money into five low-toll investment options, namely: a bond fund, a small-cap fund, an S&P 500 index fund, an international stock fund, and a fund that invests in specially issued Treasury securities. The returns you get from these investments will be accessible when you retire.

7. Guaranteed Income Annuities ("GIAs")

Alternatively, you can purchase GIAs to create your own pension. For this, you will need to trade a huge amount of coin at retirement and buy an immediate annuity. This means you get a monthly payment for life. Or you tin can opt for deferred income annuities, where yous pay bits of the annuity over fourth dimension to become monthly payment post-retirement.

All-time Savings Accounts for Retirement

There is a litany of retirement savings accounts that y'all can get. But as earlier mentioned, y'all need to choose one that is based on your employment situation and your future goals. With this in mind, nosotros would rank the following as the best savings accounts for any retiree.

5. IRA

This is a good pick considering you lot can too use it to purchase an near limitless number of investments similar stocks. It besides doesn't come up with tax deductions until you lot withdraw the money at retirement. The downside of an IRA is that the withdrawals tend to be very costly because of income tax deductions.

four. Guaranteed Income Annuities ("GIAs")

This is besides a great plan, mostly considering it cuts through all the taxation red tape. With GIAs, y'all can choose to simply pay tax for the annuity'southward earnings.

3. The 401(k)

The 401(k) is a handy retirement savings programme, particularly if you are not very practiced at saving up once you get coin in your account. With this plan, you can only schedule coin directly from your paycheck and have information technology invested automatically before it e'er gets to you.

2. Solo 401(one thousand)

If you lot take a small business owner or are self-employed and take no employees, this is better than a Elementary IRA, because yous can invest more than into it. It may however be a bit complex to set up.

1. Roth IRA

This is the king of retirement saving accounts. For the fact that you can run information technology as an private, have the gamble to avert taxes on all money withdrawn, and still have the flexibility to accept out contributions at any time without taxes or penalties, a Roth IRA is certainly an impressive choice.

Retirement Fund vs Savings Account

Retirement funds, also known as pension funds, are investment options that allow an private to save a certain portion of their income for their retirement. So, while these ii terms may appear similar, it is important to note that retirement funds are reinvested on your behalf, and the proceeds obtained from their reinvestment are what you greenbacks out at retirement. Retirement savings on the other hand are pure savings, left in the business relationship to accrue interest which y'all can withdraw at retirement.

Source: https://www.askmoney.com/budgeting/five-best-retirement-savings-accounts?utm_content=params%3Ao%3D1465803%26ad%3DdirN%26qo%3DserpIndex

0 Response to "what percentage of salary should go to savings"

Post a Comment